Using Genetic Algorithms to Find Technical Trading Rules

Franklin Allen, Risto Karjalainen | Journal of Financial Economics 51 (1999)

download paper here

Genetic Programming Review

Conclusions

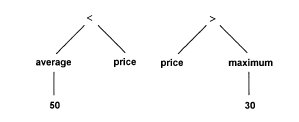

- Solution candidates are represented as hierarchical compositions of functions (not bit strings).

- Successors of each node provide the arguments for the function identified with the node.

- The terminal nodes correspond to the input data.

- The entire tree is evaluated, recursively from the root node, as a function.

- To find out whether optimal rules composed by GA's can be used to forecast future stock returns.

- Logical combinations of simple rules that look at moving averages and maxima and minima of past prices from 1929 - 1980.

- S&P 500 is the benchmark.

- Algorithm goal is to classify each trading day as being either:

- 'in' the market: earning the market rate of return.

- 'out' of the market: earning the risk-free rate of return (this is the one-month T-bill rate of return).

- Trading strategy:

- if ( ( the current state is 'in' ) && ( the trading rule signals 'sell' ) )

- switch to 'out'

- if ( ( the current state is 'out') && (the trading rule signals 'buy' ) )

- switch to 'in'

- else

- stick with current state

- Functions return either Real or Boolean values:

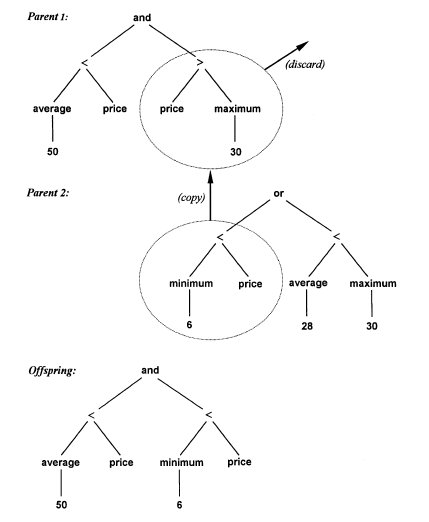

- Crossover is implemented by random selection of parent nodes:

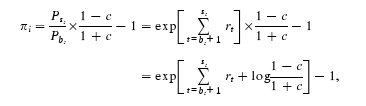

The Fitness Function

where...

Psi, Pbi = sell / buy price

c = one - way transaction cost expressed as % of price

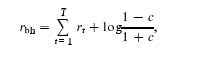

where...

T = number of trading days

Ib(t), Is(t) = buy / sell indicator variables

n = number of trades

The Algorithm

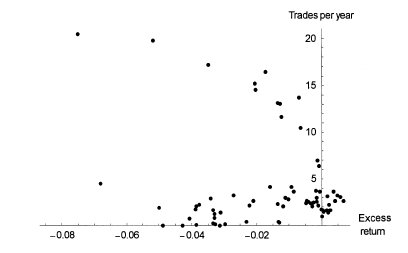

Results

*transaction costs of 0.25%

*transaction costs of 0.10%

- Fitness of a rule is computed as the excess return over the buy-and-hold strategy during a training period.

- Again, trading rules are applied to each trading day to divide the days into periods of 'in' (market return) or 'out' (risk-free return).

- Single trade return computed as:

where...

Psi, Pbi = sell / buy price

c = one - way transaction cost expressed as % of price

rt = log Pt - log Pt - 1

- Continuously compounded return for a trading rule is computed as:

where...

T = number of trading days

Ib(t), Is(t) = buy / sell indicator variables

n = number of trades

- Return for the buy-and-hold strategy is computed as:

- Finally, the fitness of the trading rule (excess return) is computed as:

- Step 1

- Create a random rule.

- Compute the fitness of the rule.

- Repeat 500 times (initial population).

- Step 2

- Apply the fittest rule in the population to the selection period and compute the excess return.

- Save this rule as the initial best.

- Step 3

- Pick two parent rules at random using fitness based selection (roulette wheel).

- Create a new rule through crossover.

- Compute the fitness of the rule.

- Replace one of the old rules by the new rule using an inverted fitness based selection.

- Repeat 500 times to produce next generation.

- Step 4

- Apply the fittest rule in the population to the selection period and compute the excess return.

- If the excess return improves upon the rule produced in Step 2, save as the new best rule.

- Stop if there's no improvement for 25 generations or after a total of 50 generations.

- Otherwise, go to Step 3.

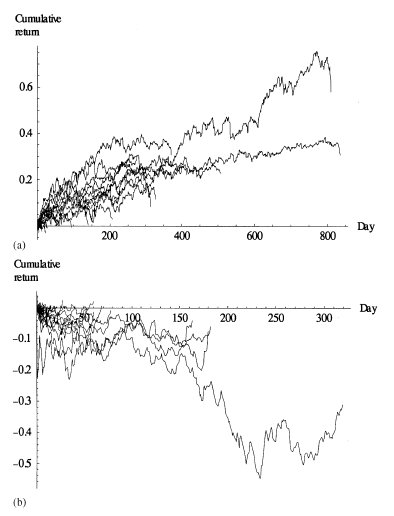

Results

*transaction costs of 0.25%

*transaction costs of 0.10%

Conclusions

- Not possible to make money after transaction costs using technical trading rules.

- Are able to indentify periods to be in the market when returns are high and volatility is low, and out when the reverse is true.